Eric Andersson, General Manager – Europe at additiv, looks at how Wealth Management-as-a-service could benefit not just the wealth industry but other sectors of the market too.

In its recent report on the financial services market, Oliver Wyman demonstrated how non-traditional players, such as PayPal and Shopify, have gone from representing 3% of the sector’s overall market value in 2010 to represent 30% in 2020.

Digital disruption from players such as these is not a threat anymore, it has already happened. And it is here to stay. The question incumbent institutions need to ask themselves is, how should they fight back? And the question non-traditional and non-financial players need to ask is how they can get in on the act? The answer to all lies in business model evolution; in changing the way they create, capture, and share value with their stakeholders.

Business model renovation for incumbent wealth managers

For incumbent wealth managers, there are multiple vectors of attack. Nimble, digitally native wealth management competitors, like Moneybox and Nutmeg, have the ability to move upstream, from retail to mass affluent and beyond, and laterally, from millennials to Gen X to boomers.

For the wealthiest clients, the technological and operational challenges of starting their own family offices have diminished.

Meanwhile, all manner of non-traditional competitors and nonfinancial players can easily and rapidly move into this space, offering wealth management alongside their existing services. Alternatively, they can offer the service embedded into their existing proposition, finding a route for those not yet actively seeking wealth management advice.

Wealth managers’ historical strategic reflexes will not cut it this time. 10-year digital transformation projects will not deliver fast enough. Similarly, building new vertically integrated propositions from the ground-up take too long. Acquisitions, like UBS’ purchase of Wealthfront, might be the answer for those with deep pockets and proven integration capabilities, but most wealth managers are not in this position.

Instead, the answer lies in Wealth Management-as-a-Service (WMaaS). WMaaS allows any company to quickly assemble new propositions using existing building blocks. WMaaS is usually positioned as a solution for companies outside of the wealth industry, but it can work for wealth managers, too.

Existing wealth managers have numerous strong competitive advantages, but they struggle to move sufficiently fast. Incumbent wealth managers enjoy the benefits of their established brands, regulatory expertise, deep investment know-how, and enduring customer relationships. But the playing field has changed.

WMaaS enables incumbents to operate at the speed of their digital competitors; to address new services, new demographics, and new geographies.

Wealth managers can assemble the propositions they need using existing plug-and-play infrastructure, dramatically cutting time-to-market. These propositions can be offered through pre-existing, white-labelled apps or embedded directly into existing channels. This is done at the same time as leveraging existing regulatory and custody capabilities to achieve scale economies, while also maximising cross-sell and customer lifetime value through the leveraging of data.

Business model enhancement for non-wealth management financial firms

Wealth managers are not the only financial firms to be under competitive and market pressure. A recent study from Simon Kucher & Partners found that of the 400 neobanks globally (also referred to as ‘challenger banks’), less than 5% are breaking even. And more established financial institutions do not fare much better, with McKinsey estimating that the average bank’s return on equity is 8% globally and that the majority of the world’s listed insurance companies make no economic profit.

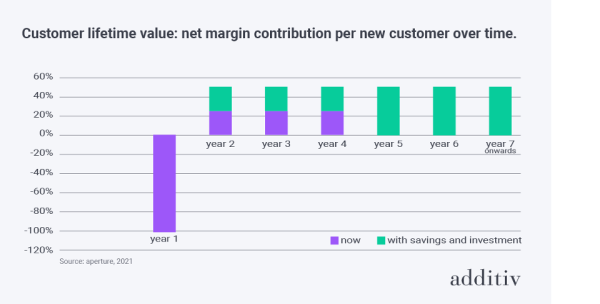

Figure 1: Customer lifetime value: net margin contribution per new customer over time. Source: aperture.

As a result, we can expect many financial service companies, who historically have not operated in wealth management, to do so to bolster their profits. Wealth management is an attractive business, with lower capital requirements and higher fees relative to their core businesses, but also presents attractive cross and upsell opportunities.

Take challenger banks, for instance. They have extremely difficult unit economics. It costs hundreds of dollars to acquire time- and attention-poor consumers. The challenger banks often only have

a narrow set of services; meaning that customer lifetime value is low, and the risk of attrition is high. Offering wealth management services adds higher-value service, increasing lifetime value and increasing the cost of the customer acquisition. Additionally, it binds the client to a journey: from earning to saving to investing, increasing stickiness.

For all financial firms, the best route to launching wealth management is also WMaaS. Not only is there a time to market advantage, but there is an expertise and capabilities gap that can be easily bridged. To be truly plug-and-play, WMaaS is not just about distribution, but the end-to-end fulfilment of wealth management services: from order management to custody to settlement.

Business model innovation for non-financial players

For non-financial players, the prize of wealth management is also to boost unit economics, but with the added advantage of being able to embed wealth management into existing journeys to increase conversion.

There are many examples of non-financial providers that could offer wealth management as part of their offerings, such as high-end retailers and super apps. All such providers should look to WMaaS. While financial firms (including wealth managers) could theoretically build these services (but should not), non-financial providers are likely to look to third parties. However, referral agreements are different from ‘embedded finance’.

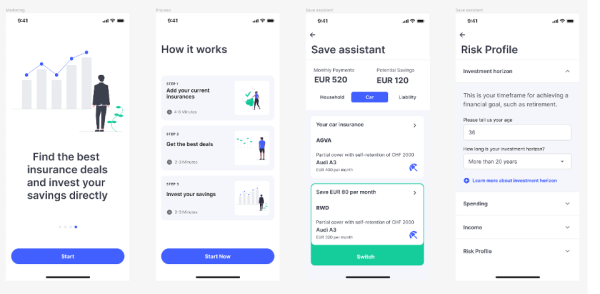

Figure 2: Embedded Wealth Solution example screens, additiv

Embedded finance is an innovative business model which oversees a brand’s leverage of existing customer relationships, insight, and engagement. The aim is to become a distributor of financial services, in this case, wealth management.

Embedded wealth management starts with the consumer’s needs. It proactively understands what job a customer is looking for to get done, like getting more return on their spare cash, and it makes it happen. It provides the right service, in the right form, at the right time. In doing so, it delivers a wonderful customer experience, but it also achieves a much higher level of conversion of cross-sell activities.

In short, we can expect digital disruption of wealth management to continue and those able to capitalise on this will be those who leverage the power of WMaaS.